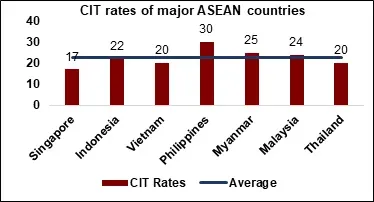

The standard Corporate Income Tax (CIT) rate in Vietnam stands at 20%. Besides the already low tax rate, Vietnam also has preferential tax rates of 10%, 15% and 17% based on the industry and the size of business. The chart below provides a comparative view of the standard CIT Rates of 7 major ASEAN economies, and in doing so, a measure of their relative business friendliness. As can be seen, Vietnam’s CIT rate is lower than the rates prevailing in other ASEAN emerging markets, thus, making the Vietnamese economy an attractive option for foreign investors looking to enter the region.

It is also important to note that the state plans on reducing the rate of taxation to 15% for micro industries and 17% for small industries. This serves as an additional step forward in Vietnam’s progress towards economic appeal.

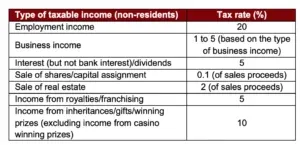

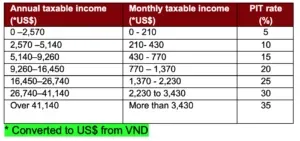

With respect to the preferential tax rates and incentives, if a manufacturing project has a minimum capital investment of US$ 260,000, they get tax reliefs. Further tax incentives are also given to high technology, textiles and automobile industry. The government also provides additional tax incentives for R&D and local employment. Personal Income Tax (PIT)–Vietnam imposes a progressive tax structure on residents while levying a flat 20% PIT rate on non-residents. The PIT structure of Vietnam is illustrated in the Tables 1and 2 below:

Table 1

Table 2